Credit cards - present and future

From their humble beginnings as store cards in the 1920s to becoming an integral part of American consumer life, credit cards have transformed how we spend, save, and perceive money, evolving significantly over the years. Culturally, credit cards have become symbols of status and identity. Premium and exclusive cards are often marketed as lifestyle accessories, emphasizing luxury and exclusivity. This strategy reflects broader societal values that equate success with material wealth and spending power.

Despite recent challenges like record high inflation, rising interest rates, increasing card debt, and delinquencies, consumer spending remains resilient and on track to grow to new highs, with credit card utilization growing rapidly.

In this article, we explore the current and future state of credit cards, examining the macroeconomic context, current trends, and future predictions.

Macroeconomics

Macroeconomically, the worst is over – dramatic inflation rates have cooled, interest rates have peaked, and economic growth continues. However, on the consumer finance side, debt has reached historic levels – the average credit card balance of American consumers reached record highs in 2023. Delinquencies (30 days past due payment) are rising and signal underlying instability in consumer debt. Were there to be a sudden reversal in economic growth or a spike in unemployment, delinquencies could surge leading to a potential credit crunch.

Interest and Inflation

As of July 2024, inflation has fallen drastically to ~3% from its peak of 9.1% in June 2022 (8% for the year). Inflation is expected to close 2024 at 2.8% and trend around 2.4% in 2025. The current target range for federal funds rate is currently 5.25% to 5.50%, a far cry from the 0% to 0.25% during COVID and 1.50 - 1.75% pre-COVID.

Promisingly, the Fed has indicated that it won’t wait for inflation to hit 2% before cutting rates, and Federal Reserve Chair Jerome Powell has stated that he doesn’t foresee a hard landing for the economy as a likely scenario.

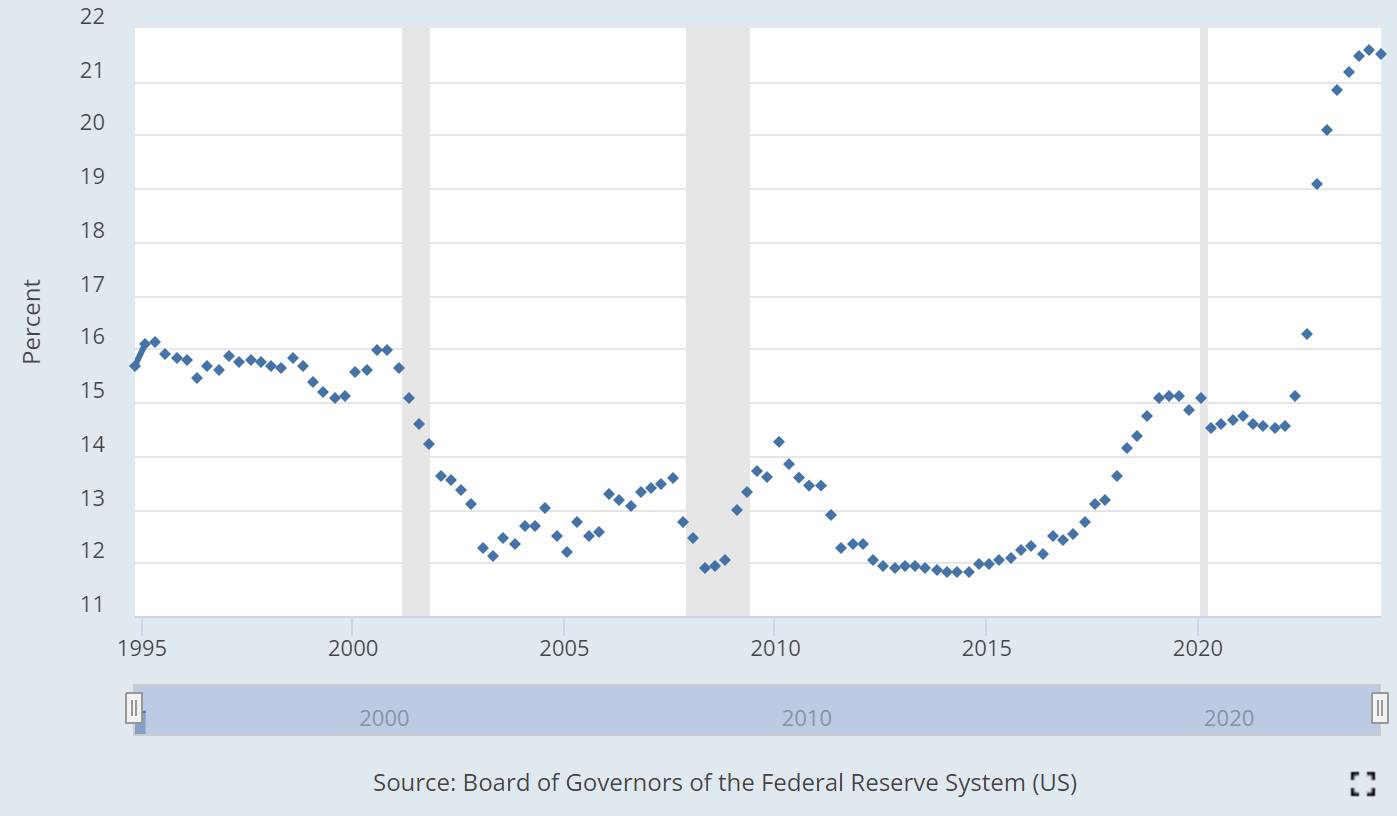

Despite this, the Fed’s rate hikes since 2022 have significantly impacted the credit card industry. From 2020 to July 2024, average credit card APR has jumped from 14% to 24.72%, driven in part by rate hikes but also corresponding increases in consumer credit risk.

As inflation levels off and Fed rates slowly retreat, we should see a gradual reversal in credit card interest rates. However, overall credit card debt as well and increasing delinquencies suggest that we are still on shaky ground.

Credit Card Debt and Delinquencies

Average credit card debt per borrower reached a new record high of $6,360 by the end of 2023, up 10% from the prior year and representing an all-time high. Simultaneously, delinquencies (30+ days past due payments) went up 50% in 2023, of which “serious delinquency” (90+ days past due) went up 59% from 4% in Q4 2022 to 6.4% in Q4 2023. Notably, these figures have risen to pre-pandemic levels, which suggests that we are breaching a more systemic longer term issue.

Naturally, demand for balance transfer offers will continue to increase, promotional 0% interest rates for a fixed period will draw in consumers looking to escape higher interest rates on their existing cards. Again, if we see a reversal in economic fortunes and unemployment rates, delinquencies could surge and lead to a self-reinforcing credit crunch.

Credit card purchase volume & interchange fees

Credit card purchase volume continues to grow, solidifying credit as a consumer staple. Recent data is hard to come by but in 2022, credit cards accounted for $5.6 trillion (53%) of the total $10.4 trillion purchase volume on general purpose credit and debit cards.

This continued growth in credit card volume is driven by several factors. First, credit cards remain the most popular payment method for online purchases, with 65% of online shoppers paying for goods or services by credit card in 2021, up from 57% a year earlier. Additionally, credit cards are the preferred payment method for in-store purchases, representing about half of total sales at the point-of-sale.

Future of Credit Cards: Innovations and Trends

Increased creativity around rewards programs

Credit card issuers will continue to become more creative with their rewards programs. As competition intensifies, balancing the cost and demand of rewards will be crucial. The Credit Card Competition Act (CCCA), if eventually passed, will put downward pressure on interchange fees and potentially lead to a reversal in premium rewards programs. This is explored in depth in my previous article on the CCCA here. Premium travel rewards also face headwinds due to overcrowding of lounges and high demand and utilization driving up costs.

Greater personalization

As competition on functional attributes of credit cards such as rewards programs reaches its local maximum and falters, personalization will be the defining factor in competitive differentiation. Issuers will need to aggressively leverage data and technology to offer customized rewards and perks tailored to individual consumer preferences, driven largely by Gen Z and Millennial demands. This approach, if done correctly, will provide new avenues for sustainable competitive differentiation while driving user engagement and reducing the churn rates which have become commonplace.

Retail partnerships

Retail partnerships will play a significant role in both reaching the local maximum of competition on rewards, and shaping the future of personalization. Issuers will collaborate with retailers to offer exclusive benefits and seamless shopping experiences.

Going beyond the card - layering new value-add features

While bundling and value-add offerings exist upmarket with large providers, pure-play credit card issuers (read: fintechs) will need to go beyond credit cards to layer additional value on top of their offerings. Many have started experimenting with integrating personal finance management (PFM) and other features to increase both perceived value and customer stickiness.